Selling covered calls

In this example the manager of a portfolio of European equities wants to achieve a higher return. His holdings have already posted gains, he is confident that the current sluggish trend will continue, and he believes the uncertainty of future returns is so minimal that he can afford to take a short position in call options.

He therefore decides to write call options on the Eurostoxx50 index. These option premiums provide immediate cash income here and now. The constraint is that if the stocks in his portfolio rise sharply, his gains will be limited. The options he writes are European options, which means that they cannot be assigned before expiry.

Strategy:

For simplicity, this example is based on a portfolio composed of just stocks and the generalisations made about them are straight forward.

The portfolio consists of two stocks, A and B, valued at 40 Euros and 60 Euros respectively. The manager holds 1,100 shares of A, which have a beta of 1.20 relative to the Eurostoxx50 index, and 600 shares of B, which have a beta of 0.75. (

Beta : a measure of the sensitivity of an asset (X) to a benchmark index (Y)).

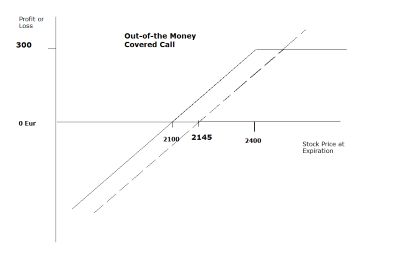

His portfolio is therefore worth 80,000 Euros (1,100 X 40

Euro + 600 X 60

Euro ). The Eurostoxx50 index is quoted at 2145 points. This portfolio is perfectly correlated with the index, since the combination of each stock’s beta weighted by its capitalisation in the basket gives an aggregate beta of 1.00.

For this portfolio, the number of call options to be sold is obtained in the following manner:

______Portfolio value_____ = __80 000 Euro__ = 3.72.

Index value X multiplier 2145 X 10

The manager, being conservative, chooses the Sep 12 2400 Call at 45.00.

Sell 4 eurostoxx50 2400 calls at 45.00 each for an immediate gain of 1,800

Euro (45.00 X 4 (number of contracts) X 10 (multiplier)).

Selling naked put options on futures

Most people are familiar with insurance brokers. An insurance broker will sell a policy (for a premium) protecting you from financial losses in case certain event occurs - like if your car is written off in an accident.

Sellers of naked puts on futures are essentially insurance brokers. They grant an insurance policy to a buyer of put options, stating they will take on the risk of the asset in question falling in value in return for a premium. If written regularly, the premium could provide a small, consistent income to the seller as long as the put option is never exercised.

Anatomy of a naked put

Obviously, the seller of a naked put does not want the underlying market to fall. Hence the first characteristic a put seller looks for is an underlying where big moves are not expected. The second condition a put seller might look for is an underlying market where there has already been a lot of uncertainty or volatility. In highly volatile market, premium of underlying assets could increase tremendously. Think of the insurance policy earlier described. What would happen to prices of home insurance policies if everyone was expecting a hurricane? And finally, the put seller will be mindful of the time the option has left to run – premium experiences time decay (i.e., fall) as the expiry approaches. Therefore a seller can sell the option and wait for its decay before buying it back at a profit.

To summarise, option sellers can benefit from three main factors: time, high volatility or lack of movement in prices.

When might selling puts be a good idea?

• When an index is at or near support and the seller’s position isneutral or slightly bullish. If neutral, the seller would sell at a strike that is out-of-the-money (OTM), i.e., an option with no intrinsic value. If slightly bullish, sell an at-the-money (

ATM ), i.e., the option trading closest to the underlying price).

• When the option contract has 20-40 days to expiry

• When the market’s volatility has risen by more than 20% of the historical volatility level.

Trade example

1. Determine your position (the example below uses German bunds). The trader in this example must beneutral or bullish when selling puts.

2. Select anexpiration (20-40 calendar days)

3. Select astrike price (if bullish one could sell ITM, if neutral

ATM , if bearish-do not sell)

4.

Sell 10 XEUR August 141.50 puts @1.60.Return on Investment (ROI) premium/strike price, or 1.60/141.5= 11.3%

5. Exits: for profit, exit by capturing at least 80 percent of 1.53 or if the contract is worth .32 cents or less. Exit for a loss if 1) the underlying bund price moves below a technical support; or 2) you have lost more than 20 percent and the premium for the option is worth 1.92 per contract to buy it back.

6. Traders should exit the option contract two to three days before expiration -Remember these are American style options and could be assigned at any time before expiration.